Following up from my previous update, I mentioned my latest PRIME US purchase was a short term punt on the news of debt renewal. It happened and the share price went up 30%.

Refinancing for PRIME (almost done)

PRIME US REIT's refinancing is almost done and I believe it can be successfully completed. Both PRIME and KORE REITs are financially stable for now. Unlike one financial blogger who terms this US REITs as "Sampan REITs", I do not think this is entirely true.

What has negatively affected these 2 US commercial REITs is the overall industry. Cashflow wise, they have been able to promptly pay their debt facilities' instalments. Therefore, I do not think they are as distressed as it seems. As a few of their properties are in US cities with stronger vacancy and Grade A status, they should be able to benefit much as US office vacancy stabilises.

Overall, I am still optimistic that these REITs can double in share price from here as they shift closer to their net asset value.

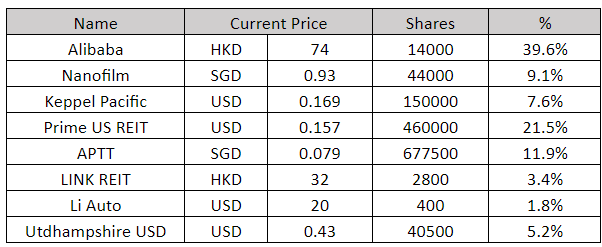

Li Auto was sold as well given the run up in prices.

Bought LINK REIT

Using the sale proceeds, I bought LINK REIT. The reasons are: largest REIT in Asia, one of the lowest leverage ratio, properties are diversified across East Asia/Australia, an internal REIT manager eliminating conflict of interest and 8% dividend yield. It surpasses all Singapore REITs and is definitely better than any Capitaland or Mapletree REIT. I would focus only on LINK REIT for Asia exposure.

With LINK REITs purchase, it does look like my portfolio is becoming a dividend portfolio; but that is because globally, the high risk free rate makes dividend stocks appealing while in Singapore our risk free rate is artifically suppressed.

No comments:

Post a Comment