Time and time again, we have been hearing from property agents that buying Singapore properties allows you to earn rental returns and capital appreciation.

Let's take this example, pay $1,000,000 for a condo unit, rent it out for 3.5k per month. Make a downpayment of $300,000 to get good returns. The maths will work out as follows.

Revenue

$3,500 x 12= $42,000

Cost

Interest on $700,000 (60% leverage) at 4.2% interest = $29,400

Rental Commission to agent= $3,500

Property Tax on 40k annual value = $4,000

Returns

$5,000 on $300,000 downpayment. Annual returns of 1.6% per annum

Capital Gains= Property Appreciation of 50% and above.

Good Financial Advice?

In my opinion, property agents using the above as financial advice are not giving the optimal solution.

Look overseas and we have REITs that give 8%-10% returns and have potentially higher capital appreciation.

What are these REITs?

LINK Reit is pherhaps the best. It is one of the largest REIT in the world, one of the lowest leveraged and is diversified across many countries such as China, Hong Kong, Singapore and Australia. Its size is larger than Capitaland and is a blue-chip company

A standard bearer of what a REIT is, Straits Times has covered it and complimented on its value creation for its unitholders. See article here

In my view LINK REIT is better than any property purchase where it is currently paying out 8% dividend per year and has a potential capital appreciation of 60%. My valuation of LINK REIT is HKD$55.

UtdHampshire REIT- Another REIT which I think its good. I have covered on this US retail specific REIT. Utdhampshire REIT sports a 9% dividend yield and has a potential capital appreciation of 60%. Target price is USD$0.70.

Overseas REITs will perform better than local condo launches

Like condo launches, the above REITs will benefit as the interest rate cut cycles happen. For those who borrow to buy condos, the interest expense of your loan reduces when interest rate are lower. This happens too for these REITs.

Hence why go for condo purchases here, when overseas so many REITs offer better dividend returns and capital appreciation. Furthermore, you do not need to go into heavy debt when owning these REITs.

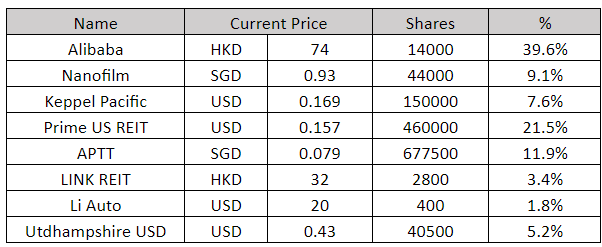

I am not a person who talks, but one who walks the talk. Over time, I have been purchasing REITs and trust such as Utdhampshire REIT, Link REIT, Asia Pacific TV Trust (APTT). I have not recommended APTT much because of its slightly higher risk profit. However, the first 2 offers great value now. LINK REIT is pherhaps the best choice because even Singaporeans would have visited its properties at Jurong Point and AMK Hub. It shows LINK REIT business is real and it provides far superior returns to buying any condo launch in Singapore now.

Disclaimer: The publication is solely for informational purposes and is not to be construed as a solicitation or financial advice as I am not a certified financial adviser. My analysis on companies covered are not an offer to buy or sell any stocks and I encourage readers to do your own "due diligence" before investing.