In March 2020, I had covered Sembcorp Marine (SMM) and lamented that given the poor O&M Industry outlook, it is likely interested bidders will pay for the company at 0.7 times its book value.

UOB KayHian (UOBKH) has recently released its brokerage valuation of SMM; valuing the company to be worth 12.5 cents (0.7 times its net tangible value at its brokerage estimated end FY21 NTA of 17.8 cents per share) and issued a sell call. This is one of the probable contributing factor to SMM share price fall over the past 2 days.

I do agree with the analyst in his projection of how much losses SMM will be incurring through to FY22. However, I realize the analyst had made mistakes in his calculation and has opened a possible investment opportunity.

UOB KayHian's Calculation Mistakes

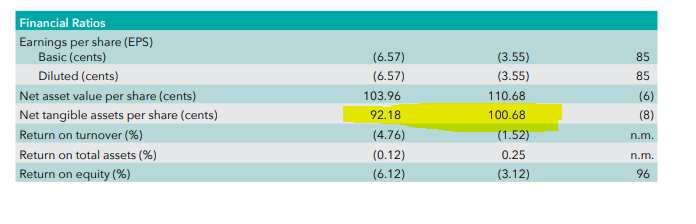

In the analyst report, SMM's estimated 2021 tangible book value is at 17.8 cents after factoring in a loss per share of 2.1 cents and 1.1 cents in each of the FY leading to it. Back of the envelope calculation means UOBKH has calculated the current tangible book value to be 21 cents per share. This is factually wrong based on SMM's published results.

In SMM's investor relation and annual report for end FY2019, they have published its net tangible asset per share to be 92.1 cents per share (see screenshot above). This is before the dilutive issuance of 5 rights for every 1 shares at 20 cents. After netting the effect of the rights dilution, the net tangible asset value of SMM share does not tally to UOB KH's report. The actual post dilution NTA is 31.95 cents per share. This is repeated in page 13 of the circular sent to shareholders in July 2020.

The True Calculated Net Tangible Asset Value

Hence factoring UOBKH's forecasted losses of 2.1 cents and 1.1 cents per share and the actual NTA of SMM; in FY21F, SMM's estimated net tangible asset value is 28.75 cents per share.

Applying a 0.7 times book value factor, SMM is valued at 20.1 cents per share.

In summary, UOBKH has greatly miscalculated SMM's estimated NTA by at least 10 cents. The analyst had calculated it to be at 17.8 cents when it should be 28.75 cents.

This signals a potential investment opportunity (upside of 35%) from the current sold down price if the 20 cents target based on UOBKH's forecast and parameters are met.

I have invested a bit into the shares today upon realizing the calculation mistake by UOBKH.

<Vested in SMM shares>