“How do I start to reach my financial goals?”

“What must I invest in?”

These are questions often asked as newcomers to the workforce embark on their goal to start saving for retirement. And the first steps to it is saving with a certain figure in mind. So how can one achieve this first financial milestone of saving, say their first $100,000? While many would think the ability to invest smartly is required to achieve this goal, the truth could not be any further.

Its more about Saving Habits than Smart Investing

In my view, if you have the goal of saving $100,000 before the age of 35 (or preferably 31), achieving your milestone depends more on how much you save than the ability to invest for wonderful returns.

Let’s use the example of “Ben” to illustrate. Following the path of most university graduates, Ben graduates and enters the workforce at the age of 25. There he attains a job with a monthly salary of $3,000 (After CPF: $2,400). Ben expects an annual 5% increment during the early stages of his career and intends to save a full 1 month of his bonus annually. In addition, being a new investor, Ben expects to invest in “safer” stocks which will yield him an annual investment returns of 4%.

Under $1,000 Monthly Expenses

As mentioned, Ben intends to keep his personal monthly expenditure to under $1,000 or about 40% of his take home pay. This is how his monthly expenditure will look like. Do note that while the insurance expense is low at $45, this is because term coverage of $200,000 and hospitalization insurance is utilized.

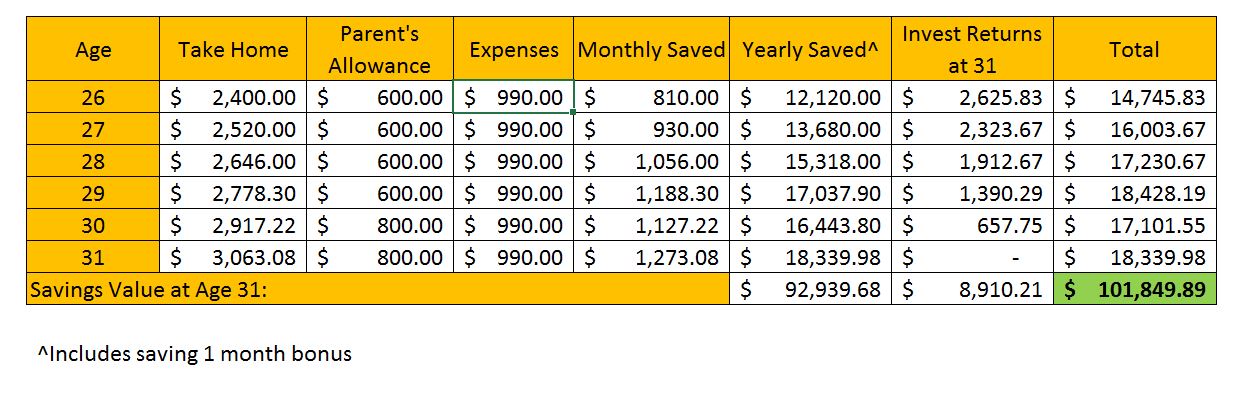

All in all, Table 2 shows how much Ben will save monthly. At the start of his working life, he is saving only about 30% of his monthly take home pay.

|

| Table 2: Saving Table at age 26 & 30 |

Based on the calculations, Ben will save $100,000 when he is 31 years old.

Analysis of how Ben achieved his $100,000

Based on Table 3, a significant portion of the $100,000 was due to Ben’s savings. In fact, only $8,910 was a result of his investment returns. To summarise, 91% of Ben’s financial milestone was due to his efforts of keeping monthly expenses low (below $1,000); enabling him to save 30-40% of his take home pay.

What if Ben had been Given Wrong Financial Advice or Spent More?

Let’s put additional thoughts to the above example. How would Ben’s milestone of $100,000 be affected if instead of spending $990 monthly, Ben spends $1,340 monthly. The reasons can vary such as instead of being advised to take Term insurance, Ben was offered Whole Life insurance (which will cost him $350 more monthly for the same coverage) or Ben simply decides to spend $350 more to pamper himself.

From a spending ratio of 30-40% of his take home pay, Ben’s spending ratio has now increased to the 43-55% range. Correspondingly, this will affect his savings ratio (a decline from an average of 39% to 26%).

|

| Table 4: Saving Amount at reduced Saving Ratio |

At age 31, Ben will only be able to save $73,991. Hence, just a decision to 'spend more' or 'an advice to choose Whole Life instead of Term' sets him back a difference of $26,000. Ben has been delayed by approximately 2 years in achieving his financial milestone of $100,000.

Conclusion

To summarise, the financial milestone of $100,000 depends greatly on what you spend and the amount you save. From Table 3, it shows just how little investment returns contributes. It is only if we take a longer term horizon, will the compounding of investment returns be substantial to contribute to our wealth building. However, for our investment returns to be significant, we need to build a large capital base and this boils down to an individual’s spending and savings habit.

Lastly, some individuals (particularly insurance agents) will dispute the later part of this post where I have “expense” the differential where Whole Life insurance is involved. It is worth noting for individuals who purchase such policy, they will never get to see their maturity sum, hence such a sum/differential should never count towards their retirement fund. Suggestions such as surrendering the policy when they are older (i.e. age 65) may then be offered; however, such a surrender comes at a penalty, and it reduces the returns of whole life insurance to the region of 2-3% per annum. If that is the case, investing the differential on your own is a much better option.

No comments:

Post a Comment