The tech sell off worldwide is something worth observing. With higher interest rates in the immediate future and central banks balance sheet run offs, investors will now demand that tech companies be profitable, becoming like other traditional companies.

The past decade of cheap money and venture capital success has allowed entrepreneurs to incubate loss-making businesses for probably the longest period ever. However all these are about to change.

Either companies become profitable or they die off

Like all boom and bust cycles, the inefficient and unprofitable ones will be weeded out. This is similar to the dot com boom era where "Mickey Mouse" companies sprang up, had unviable business models, raised capital with alluring stories, CEOs became a poster child and then kaput. We have seen this in the 2000s before and I didn't like the ending

Of course, there will be survivors who turn out to be dominant forces in the next decade. However, they had a sustainable business model that was scalable to start with. And it seems the likely few are Tesla and Airbnb. (their share prices will follow similar to what Microsoft went through in 2000s)

How to be profitable?

Its simple- either increase your revenue or cut your cost. Netflix is now attempting to increase its revenue by raising its monthly subscription fees in its mature markets. Gone will be the days where there are free shipping for small value purchases, cyber vouchers given out daily and deep discounts (I am referring to what Sea Group and Grab have been doing).

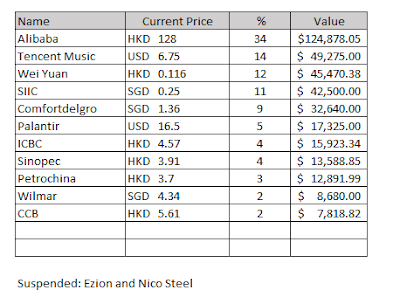

Of course, the other way is to cut cost. Taking Palantir as an example: In its latest quarter, it earned about USD$392 million, however employee expenses made up approximately US$190 million (about 48%). This is a lot higher than the traditional companies where employee costs form less than 20% of revenue. Palantir definitely has to cap its employee expense as it grows; otherwise, Palantir will go bankrupt or have to issue an expensive round of share dilution. Sea Group and Grab too are in this category.

Cost cutting measures will involve to stagnate your tech worker's salaries or trim them. Everyone now knows the best industry to work at is Tech - chief reason the remuneration is good. However, the good times aren't going to last and I expect the Tech workforce to experience trying times soon.

The era of accommodative monetary policy is gone. Tech companies have to tighten their belts and be profitable, otherwise they will be joining the tech graveyard of the 2000s.

Who are the winners?

Truthfully I want to say it is the China Tech companies. They have built up a profitable model, are sustainable and using their free cash to generate new products and segments. However, they have been hampered by their own government making them less competitive and unable to spread their influence of "Chinese Tech and Innovation" when fighting with regional competitors.

In the era of monetary tightening, they are in my '"winner list" with their profitable business model. Just look at the difference between Tencent Music and Spotify current financial results. Both are leaders in their respective markets and are serving about the same population market size. However Tencent Music is at least 4 times more profitable than Spotify.

Furthermore with China now going the other way of having monetary accommodative policies, they are in a better standing to fight global tech companies.

If tech workers want to keep their job, working in a Chinese Tech Company is the safest bet.

And the Losers?

I feel the ride hailing and food delivery industries are in a serious problem. Ride hailing is a low margin business and worldwide all ride hailing companies are loss making. It will be difficult for them to be profitable unless they undergo retrenchment and price hikes (the latter will make them less attractive options to consumers when compared to the cab business).

Food delivery too has the issue of being too cheap to the expense it is negative in profits. The plastic/ Styrofoam used in the Asian markets is very worrying environmentally. However, governments are reluctant to regulate/tax business on this either due to worries of causing loss of jobs or simply angering their voters.

I don't expect many food delivery and ride hailing entities to survive this current cycle of monetary tightening unless central banks turn tail on their current interest rate trajectory.