On SGX, a stock screener function is avaliable and dividend stocks can be filtered. I will be weighing my thoughts on the 5 highest SGX dividend stocks and if it is sustainable. I have excluded PRIME US and KORE REIT which SGX listed as No 2 and No 3 because their dividends have been cut.

1) World Precision Machinery (Yield 19%), WPM

A china precision stock which focuses on metal stamping products. The company distributes a payout ratio of 30% of earnings as dividends. However, first quarter the company reported a loss and this has spooked the market. Looking to this year's results, it is likely dividends will be cut if company follows its 30% payout ratio policy.

WPM is a proxy to the Chinese Manufacturing health. China's manufacturing is declining.

However, if investors want to bet that Chinese manufacturing will recover, WPM is a good bet. The company's balance sheet is relatively healthy and I believe should China recover, WPM will resume dividends at 10+% at current cost price

2) Pacific Century Developments (Yield 14%), PCRD

A large shareholder of HK largest teleco, PCCW/HKT, part owner of FWD insurance and Viu (OTT). PCRD generates dividends from the dividends decalred by its asosciate companies. In 2024, iPCCW/HKT generated a bumper dividend and PCRD then shared the earnings as dividend to shareholders. PCRD is a holding company which just holds investments with no main business on its own, similar to Taiwan's Hotung Holding.

How much PCRD distributes as dividend annually depends on the performance of PCCW in HK and Viu. The current strucutre of PCRD is that it is largely held by Pacific Century Group with Richard Li at the helm. PCRD is structured to be milked as a cash cow providing the cash to its parent, Pacific Century, to finance its operations.

Hence as long as the structure remains, it will definitely be a top dividend stock for shareholders.

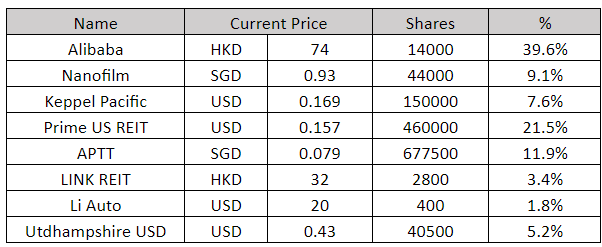

3) Asian Pay TV Trust (Yield 13.2%), APTT

APTT is in the TV/Broadband business in North/Central Taiwan. Its annual dividend is 1.05 cents.

With dividend forming only 15% of its free cashflow with the remaining used to pay down its large debts. The trust is highly geared but i believe it will not affect its dividend. I foresee a continous issuance of 1.05 cents dividend. Its TV business is declining but the remaining cashflow generated from its broadband business is able to support current dividend.

4) HPH Trust USD (Yield 13%), HPHT

The trust pays a high and fixed payout ratio. It is in the business of Hong Kong Terminal Port operations. The port operations is currently in an upcycle with supply outstripping demand. This is why HPHT is earning good profits and in turn distributing it out as dividends.

It is in a cyclical industry. Hence I do not view the current dividend as sustainble. It depends on the dynamics of Hong Kong's port supply/demand.

5) ARA US Hospitality Trust (Yield 11.8%), ARAHT

The trust is in the 3 and 4 stars hotel business in USA, catering to the mid end business and tourists. While it sports brand names such as Marriott, Hilton and Hyatt, the tier of the brands ARAHT has is for consumers of the middle income level. Its hotel occupancy has been low, but churns out good profits because unlike office/malls, hotels occupancy do not need to be sky high to maintain profits.

To delever itself, the trust has been selling a few properites such as Hyatt House. The trust has a sightly high leverage and is facing an increasing cost of debt due to US Fed interest rate upcycle (now in the region of 5.7%). However, I feel the dividend is sustainable. The reason why its dividends places it in top 5 is because Mr Market is worried about its declining profits/earnings due to high interest expense and valuation decline due to the need to set higher discount rates. However, once the cost of debt falls due to the reduction in US Fed interest, its dividend can still be maintained.

Investors should expect a drop in annual dividends this year. This is because the trust has to conserve some cash. Secondly, there is a change in ownership from ARA to the Tang family of Chip Eng Seng. It is likely some cash will be saved so that when the upcycle in US hotels happens, the Tang Family will inject Chip Eng Seng US hotels into ARA portfolio to monetise it. The injection may mean ARAHT has to pay out via cash/borrowings/share placement

Summary

To me, no 2 and 3 will likely continue to dish out good dividends. No 5 is a mixed bag because there could be an undertone that ARAHT could be conserving cash and then using it to monetise the new owner's US hotel assets via an injection into the stapled trust.

No 1 and 4 are dependent on the industries they are in, so earnings/dividend are cyclical.